Will This Stock Be the Next Retail Sector Short Squeeze After American Eagle?

Following American Eagle’s (AEO) rapid retail rally on the backs of a short squeeze and a viral ad campaign featuring actress Sydney Sweeney, another big name from the retail sector may be joining the short-squeeze bandwagon.

With nearly 21% of its float sold short based on MarketBeat data, shares of Birkenstock (BIRK) may be the next target of short squeezers.

About Birkenstock

Founded way back in 1774, Birkenstock is best known for its sandals and shoes featuring anatomically contoured cork footbeds designed for foot health and comfort.

Valued at a market cap of $9.3 billion, BIRK stock is down 12.8% on a year-to-date basis.

But unlike these three highly shorted stocks, where a squeeze may not be sustainable, Birkenstock’s story can be different. Why? Let’s find out.

Strong Fundamentals

Birkenstock is a profitable company with a growing top line and expanding “footprint.”

In its fiscal Q2, the company reported revenues of €574.33 million, up 19% year over year. Earnings also increased 46% to €0.56 per share from €0.38 per share in the year-ago period.

Analysts are expecting a continuation of this growth trend, with its forward revenue and earnings growth rates pegged at 20.01% and 78.15%, both of which are much higher than the sector medians of 2.91% and 6.82%, respectively.

Although Birkenstock's net cash from operating activities denoted an outflow of €18.3 million in Q2, the company still managed to bolster its cash balance from the previous year to €235.4 million. This was €175.7 million at the end of Q2 2024. Further, the cash balance was also higher than the company’s short-term debt levels of €38.8 million.

Notably, Birkenstock is set to report its Q3 2025 results on Aug. 14 before the market opens. Analysts expect $0.70 in earnings per share on revenue of $736.56 million.

Growth Driven By Expansion and Demand Strength

Birkenstock continues to make notable strides in international expansion, accompanied by a steady improvement in profitability metrics.

To that end, recent capital expenditures to expand manufacturing capacity are beginning to yield results. As demand grows, the company’s ability to leverage its scaled operations is contributing meaningfully to gross margin enhancement, with this trend likely to persist if sales momentum remains intact.

Speaking of sales momentum, the Asian market presents substantial long-term potential. Although the region currently accounts for less than 10% of total revenue, sales rose 30% year-over-year to €48 million. The company also opened new stores in Japan, China, and India, increasing its presence in the region to 30 locations.

Encouragingly, full-price sell-through remained above 90%, and there is no evidence of demand being hurt by anticipated price increases due to tariffs. This suggests strong organic demand and reinforces Birkenstock’s pricing power.

Finally, the direct-to-consumer (DTC) channel is emerging as a critical growth lever. Revenue from this segment grew 19% year-over-year to €140.71 million.

Collectively, these factors position Birkenstock for continued margin expansion and sustainable growth, particularly through its DTC strategy.

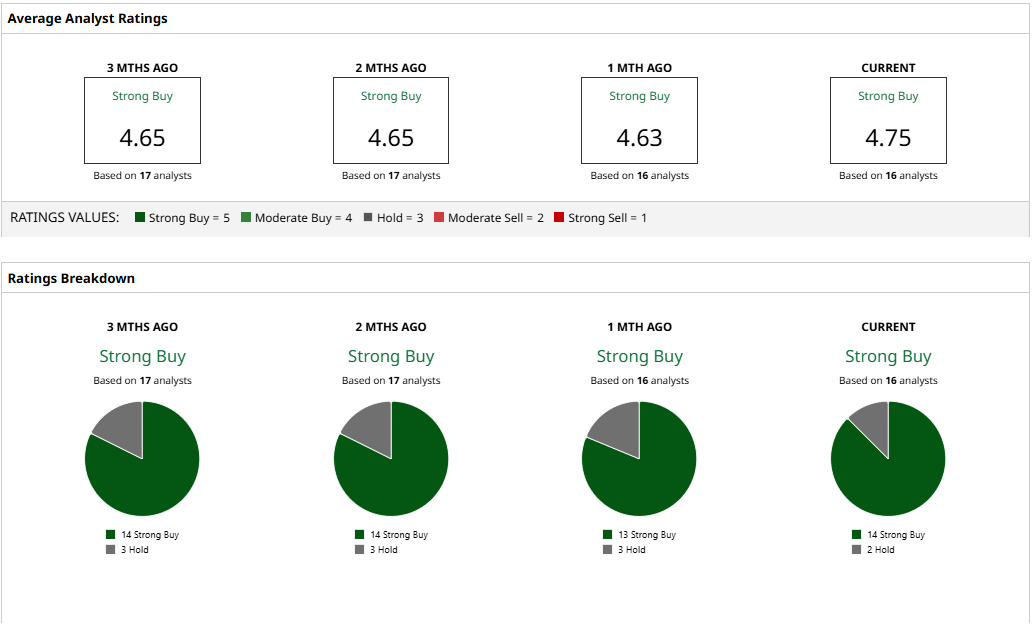

Analyst Opinions on BIRK Stock

Analysts have given BIRK stock a consensus “Strong Buy” rating with a mean target price of $68.88. This denotes upside potential of about 38% from current levels. Out of 16 analysts covering the stock, 14 have a “Strong Buy” rating and two have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.